HSBC MPF Default Investment Strategy

What is DIS?

The Default Investment Strategy (DIS) is a standardised and fee-controlled MPF investment strategy that was applied since from 1 April 2017 as the "default" investment strategy in all MPF schemes in Hong Kong. It replaced the different default investment strategies employed by different MPF schemes prior to 1 April 2017. From now on, MPF members joining an MPF scheme without providing a valid investment choice will have their monies invested in accordance with the DIS.

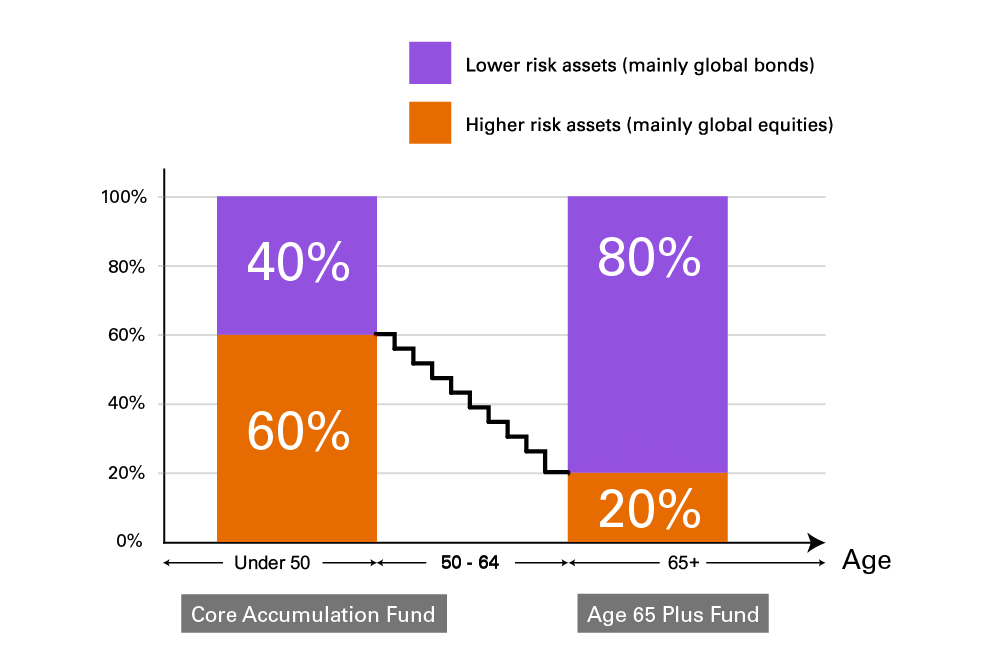

The DIS consists of 2 Constituent Funds, the Core Accumulation Fund (CAF) and the Age 65 Plus Fund (A65F). Both funds adopt a globally diversified investment approach, with the CAF investing 60% of its assets in higher risk assets such as equities and 40% in lower risk assets such as global bonds and money market instruments. The A65F has 20% of its assets invested in higher risk assets, and 80% in lower risks assets.

DIS contains an automatic de-risking feature, under which, members who are below age 50 investing in DIS will have their new contributions and accrued benefits 100% invested in CAF. In general, when a member turns 50, their accrued benefits and new contributions will automatically be partially allocated to the A65F annually on their birthdays until they reach 64, when the entire accrued benefits will be invested in the A65F. This is illustrated by the diagram and the DIS de-risking table.

Another key feature of the DIS is that both the CAF and A65F are subject to a management fee cap of 0.75% of the net asset value of the fund each year (measured on a daily basis). Furthermore, there is an additional cap of 0.2% of net asset value on the recurrent out-of-pocket expenses in operating the funds.

While the DIS has been intended for members who have not made any investment choices before, it may also be an appropriate investment option for you if the features of it fits your circumstances. The DIS is available as a standalone investment option that you may choose explicitly, or you may also choose to invest in the CAF and A65F separately.

| Age | Core Accumulation Fund ("CAF") | Age 65 Plus Fund ("A65F") |

|---|---|---|

| Below 50 | 100.0% | 0.0% |

| 50 | 93.3% |

6.7% |

| 51 | 86.7% |

13.3% |

| 52 | 80.0% |

20.0% |

| 53 | 73.3% |

26.7% |

| 54 | 66.7% |

33.3% |

| 55 | 60.0% |

40.0% |

| 56 | 53.3% | 46.7% |

| 57 | 46.7% | 53.3% |

| 58 | 40.0% | 60.0% |

| 59 | 33.3% | 66.7% |

| 60 | 26.7% | 73.3% |

| 61 | 20.0% | 80.0% |

| 62 | 13.3% | 86.7% |

| 63 | 6.7% | 93.3% |

| 64 and above | 0.0% | 100.0% |

| Age | Below 50 |

|---|---|

| Core Accumulation Fund ("CAF") | 100.0% |

| Age 65 Plus Fund ("A65F") | 0.0% |

| Age | 50 |

| Core Accumulation Fund ("CAF") |

93.3% |

| Age 65 Plus Fund ("A65F") |

6.7% |

| Age | 51 |

| Core Accumulation Fund ("CAF") |

86.7% |

| Age 65 Plus Fund ("A65F") |

13.3% |

| Age | 52 |

| Core Accumulation Fund ("CAF") |

80.0% |

| Age 65 Plus Fund ("A65F") |

20.0% |

| Age | 53 |

| Core Accumulation Fund ("CAF") |

73.3% |

| Age 65 Plus Fund ("A65F") |

26.7% |

| Age | 54 |

| Core Accumulation Fund ("CAF") |

66.7% |

| Age 65 Plus Fund ("A65F") |

33.3% |

| Age | 55 |

| Core Accumulation Fund ("CAF") |

60.0% |

| Age 65 Plus Fund ("A65F") |

40.0% |

| Age | 56 |

| Core Accumulation Fund ("CAF") | 53.3% |

| Age 65 Plus Fund ("A65F") | 46.7% |

| Age | 57 |

| Core Accumulation Fund ("CAF") | 46.7% |

| Age 65 Plus Fund ("A65F") | 53.3% |

| Age | 58 |

| Core Accumulation Fund ("CAF") | 40.0% |

| Age 65 Plus Fund ("A65F") | 60.0% |

| Age | 59 |

| Core Accumulation Fund ("CAF") | 33.3% |

| Age 65 Plus Fund ("A65F") | 66.7% |

| Age | 60 |

| Core Accumulation Fund ("CAF") | 26.7% |

| Age 65 Plus Fund ("A65F") | 73.3% |

| Age | 61 |

| Core Accumulation Fund ("CAF") | 20.0% |

| Age 65 Plus Fund ("A65F") | 80.0% |

| Age | 62 |

| Core Accumulation Fund ("CAF") | 13.3% |

| Age 65 Plus Fund ("A65F") | 86.7% |

| Age | 63 |

| Core Accumulation Fund ("CAF") | 6.7% |

| Age 65 Plus Fund ("A65F") | 93.3% |

| Age | 64 and above |

| Core Accumulation Fund ("CAF") | 0.0% |

| Age 65 Plus Fund ("A65F") | 100.0% |