Table of contents

General rules

Pay contributions in full by the deadline

You have to submit contribution details and make contributions for your employees once every payroll cycle (also known as contribution period) in full on or before the relevant contribution day.

In general, for monthly-paid non-casual employees, contributions are to be paid by the employer on or before the 10th day of each calendar month, following the end of the contribution period. For example, the contributions for the contribution period of 1-31 January should be paid on or before 10 February.

However, if the contribution day falls on a Saturday, public holiday, or gale or black rainstorm signal, the contribution day will be postponed to the following business day that is not a Saturday, public holiday, or gale or black rainstorm signal.

Calculate mandatory contributions correctly

Under MPF legislation, employers and employees are required to each make mandatory contributions of 5% of the employee's relevant income*. In other words, the amount of mandatory contributions for each employee is comprised of 2 portions: the employer's mandatory contributions for the employee and the employee's mandatory contributions out of their own pocket.

| Employer's mandatory contributions |

Employee's mandatory contributions |

|---|---|

| = 5% of the relevant income of the employee |

= 5% of the relevant income of the employee |

| Employer's mandatory contributions |

= 5% of the relevant income of the employee |

|---|---|

| Employee's mandatory contributions |

= 5% of the relevant income of the employee |

*In calculation, the amount of mandatory contributions is subject to the minimum and maximum relevant income levels. MPFA reviews the minimum and maximum relevant income levels regularly, so please refer to the latest minimum and maximum relevant income levels published at MPFA's website at www.mpfa.org.hk.

Report contribution details

When you are remitting mandatory contributions to us, remember to complete and submit a remittance statement, either in paper or electronic format. The remittance statement should include contribution details such as the relevant contribution period, relevant income and contribution amounts of each of your employees.

If there's a discrepancy between the contribution amount calculated according to the relevant income and the contribution amount reported by you on the remittance statement, we will, based on the relevant income provided on the remittance statement, calculate and allocate the contributions to your employees' MPF accounts accordingly.

Consequence of failing to pay contributions in full and on time

Failure to pay mandatory contributions in full and on time to a MPF service provider incurs a 5% surcharge on the outstanding mandatory contributions, along with the possibility of a financial penalty and even imprisonment. Refer to the MPFA website at www.mpfa.org.hk for details.

Ways to report contributions

HSBC MPF provides the following options for you to submit remittance statements. Simply indicate your choice of reporting in the Employer Application Form and we will make arrangements accordingly.

1. Paper-based remittance statement

For first-time remittance statement submissions, you have to fill in the contribution details of your existing employees in the 'Existing Employees Section'. The information required includes the employee's name, HKID card or passport number, contribution period and relevant income, amount of mandatory contributions and voluntary contributions.

Once we have processed your contributions, the latest contribution details of your reported employees will be pre-printed in the 'Existing Employees Section' for the remittance statement afterwards. If there are changes to the relevant income or employment status of your existing employees, you'll need to update the details in the 'Existing Employees Section' of the statement.

For new employees, you'll need to complete the 'New Employees Section' and arrange to make first contributions. Refer to the 'First contributions' section for details.

Remember to sign under the 'Declaration' section and provide a company chop on paper-based remittance statements.

Any completed remittance statements together with any cheque payments can be sent to the MPF department through the authorised channels for processing.

Authorised channels include:

The Hongkong and Shanghai Banking Corporation Limited

PO Box 73770 Kowloon Central Post Office

Or you may also place your documents in MPF Drop-In Box at designated branches.

Drop-in boxes have been set up at designated branches for the collection of MPF documents submitted by customers, such as paper remittance statements and any cheque payments. Submission of documents via the drop-in box will be forwarded to the MPF department for processing directly.

Any channels other than the channels specified above are regarded as unauthorised channels. Submission of MPF documents to unauthorised channels include:

- Staff at service counters at branches

- Branches without the MPF Drop-In Box

- Other collection boxes at branches (eg collection boxes for cheque payments).

NOTE

Employers and the self-employed should not hand any MPF documents (in particular for those paper remittance statement and cheque payment that must be submitted on-time according to the MPF legislation) to unauthorised channels.

Any submission of MPF documents to unauthorised channels will not be forwarded to the MPF department for processing and it may take longer for the documents to be transferred. While the receipt date by the MPF department will be stamped only when the documents reach the MPF department, employers and/or self-employed persons should note that this will result in a delay in receiving and processing paper remittance statements or other instructions by the MPF department.

Failure to pay mandatory contributions in full and on time to a trustee incurs a 5% surcharge on the outstanding mandatory contributions, along with the possibility of a financial penalty and even imprisonment by the MPFA. Refer to the MPFA website www.mpfa.org.hk for details of offences and penalties.

2. Electronic remittance statement through the Business Internet Banking (BIB) MPF Service

You can make use of our BIB MPF Service to manage contribution arrangements. Create records of your employees and provide the required information of each employee including the date joined, date of birth, amount of relevant income and any voluntary contributions. The mandatory contribution will be automatically calculated based on the employee's relevant income you have provided. A full list showing the contribution details of each employee will be generated for your validation before submission.

Find out more about how BIB MPF Service can help you. Visit our website for a service demonstration.

3. Other electronic means

You may use a format that is mutually-agreed between us, or you may use an external payroll administration software to manage your MPF administration. Given that the required contribution details are included in such electronic format that is compatible with ours, we will accept it for contribution processing.

4. Blank remittance statement

In case you fail to receive the pre-printed remittance statement or encounter any problem in submitting contribution details via electronic platforms, you're advised to make use of the blank remittance statement form, Remittance Statement - Non-daily Contribution, to make your reporting. You can click here (employers) to download or call our customer service representative to obtain a copy.

Remember to sign under the 'Declaration' section and provide a company chop on the paper-based remittance statement.

Points to note for reporting contributions

- When you are reporting contribution details, remember include all your new and existing employees onto the remittance statement even if their relevant income is zero.

- Paper-based remittance statements should be signed by the authorised person of the employer. If there is a change in authorised persons or change in authority level, notify us by returning a completed 'INY1 - Authorised Signatures Specimen (Employer)' form. Use this form to update the authority level and limit in making contribution payments, benefit payments and placing reserve account fund switching transaction.

- Make sure there is enough postage and allow for sufficient mailing time prior to the contribution day if you send the remittance statement to us by post. Failure to pay mandatory contributions in full and on time to an MPF service provider incurs a 5% surcharge on the outstanding mandatory contributions, along with the possibility of a financial penalty and even imprisonment.

- Regardless of whether the contributions are for your existing employees or are the first contributions for your new employees, if you're due to make mandatory contributions, but their records are not yet shown in the paper-based or electronic remittance statement, you must report the mandatory contributions for your employees under the 'New Employees Section' of the remittance statement and settle the contributions on time.

You should not wait until their records are shown in the remittance statement before making contributions. If you fail to receive paper-based or electronic remittance statements, you can report the contributions with blank remittance statements and pay the contributions in full. Failure to receive the pre-printed remittance statement or software problems may not be a sufficient reason for appealing the surcharges. - The contribution amount provided on the remittance statement should be rounded off to two decimal places (if applicable).

Payment methods

Remittance statement submissions should always come with the payment of MPF contributions. You can choose to pay the contributions either by cheque or direct debit authorisation. Submit clear, correct and complete remittance statements and pay your employees' mandatory contributions in full on or before the contribution day. Refer to the 'General Support' section below for details on MPF document submission.

1. Cheque payment

If you're using cheques to pay contributions, it's important for you to submit a valid cheque with clear and correct information. The contributions can be paid by a crossed cheque with Employer ID and contribution period marked at the back. You may refer to the following payee name for reference:

| Scheme name |

Cheque payable to |

|---|---|

| HSBC Mandatory Provident Fund - SuperTrust Plus |

'HSBC MPF SuperTrust Plus' or 'HSBC Provident Fund Trustee (Hong Kong) Limited A/C HSBC Mandatory Provident Fund - SuperTrust Plus' |

| Scheme name |

HSBC Mandatory Provident Fund - SuperTrust Plus |

|---|---|

| Cheque payable to |

'HSBC MPF SuperTrust Plus' or 'HSBC Provident Fund Trustee (Hong Kong) Limited A/C HSBC Mandatory Provident Fund - SuperTrust Plus' |

Payment types such as bearer cheques, cash, cashier orders or demand drafts are not accepted as method of payments. Cheques with incorrect or incomplete information will be treated as invalid and will not be accepted. Employers are required to re-submit a crossed cheque with correct information on or before the contribution day. Below are some examples:

| Items |

Invalid cheque |

|---|---|

| Payee name |

Incorrect / Missing |

| Date |

Outdated / Post-dated / Missing / Incomplete / Illegible |

| The amount in words and figures |

Not matching / Missing / Incorrect |

| Authorised signature / Drawer's chop |

Missing |

| Amendment |

Missing signature and drawer's chop |

| Items |

Payee name |

|---|---|

| Invalid cheque |

Incorrect / Missing |

| Items |

Date |

| Invalid cheque |

Outdated / Post-dated / Missing / Incomplete / Illegible |

| Items |

The amount in words and figures |

| Invalid cheque |

Not matching / Missing / Incorrect |

| Items |

Authorised signature / Drawer's chop |

| Invalid cheque |

Missing |

| Items |

Amendment |

| Invalid cheque |

Missing signature and drawer's chop |

2. Direct debit authorisation

You can also choose to pay your contributions through direct debit. Simply complete and return the 'Direct Debit Authorisation' form for our processing.

| Scheme name |

Direct Debit Authorisation Form |

|---|---|

| HSBC Mandatory Provident Fund - SuperTrust Plus |

IN14 |

| Scheme name |

HSBC Mandatory Provident Fund - SuperTrust Plus |

|---|---|

| Direct Debit Authorisation Form |

IN14 |

Points to note for payment methods

- The calculation of contributions in the remittance statement must be accurate and the amount stated in the statement should tally with the cheque or direct debit amount.

- Make sure there are sufficient funds in your bank account for cheque settlement or direct debit. Also, make sure the amount payable does not exceed your bank limit for direct debit.

Information received after contributions

Confirmation of MPF contributions

A 'Confirmation of MPF contribution' will be sent to you by mail if we receive contribution details via paper-based remittance statement or other electronic means. It lists out the actual amount of mandatory contributions and any voluntary contributions made by employer and employees.

A 'Fund purchase confirmation' in electronic format will be sent to you by email if we receive contribution details via electronic remittance statement of our BIB MPF Service. It lists out the actual amount of mandatory contributions and any voluntary contributions made by employer and employees.

Overpayment

The calculation of overpayment is based on the relevant income that you reported for employees on the remittance statement. Overpayment is the part of paid contributions exceeding the required mandatory contributions of the employee's relevant income. If there is any overpayment, we'll issue an 'Overpaid/Overstated Mandatory Contribution Report'. Any overpaid/overstated amount will not be invested into the employer or employee's account. Employers can choose to use the uninvested overpaid amount to offset future contributions or request for a refund from us. However, if we do not receive any instructions from you, the uninvested overpaid amount will be kept in your MPF scheme account without interest.

Unpaid/underpayment

Paying contributions in full on or before the contribution day is vital. In case of outstanding mandatory contributions, if the contributions are underpaid or unpaid, we're obliged to report the case to the MPFA according to MPF legislation.

The following situation will be considered as unpaid:

- No remittance statement was received on or before the contribution day

- The record of an employee, who is still under employment, showing on the remittance statement has been crossed out

- The relevant income is left blank and the mandatory contribution has been crossed out on the remittance statement in respect of an employee who is still under employment

- The relevant income and mandatory contribution sections are left blank on the remittance statement in respect of an employee who is still under employment

The calculation of underpayment is based on the relevant income that you reported for the employee on the remittance statement. If the paid amount is less than the required mandatory contribution of employee's relevant income, it will be treated as underpayment.

For employers who have not paid their contributions, we'll send them a 'Mandatory Contribution Reminder' by mail to remind them to settle the payment as soon as possible.

For underpayment, we will send a 'Mandatory Contribution Discrepancy Bill' to employers for them to provide the missing details and arrange remittance of the shortfalls.

Both unpaid and underpaid mandatory contributions are classified as default contributions. MPFA may impose a 5% surcharge on the outstanding mandatory contributions, along with the possibility of a financial penalty and even imprisonment. Even if the unpaid and underpaid mandatory contributions are subsequently settled after the contribution day, MPFA may still impose 5% surcharge on the late payment. Employers may also be liable for financial penalties, fines and imprisonment.

Points to note for overpayment/unpaid/underpayment

If the overpayment of mandatory contributions includes employee portions of contributions, you're required to refund the employee portion to your employees as soon as possible.

If the overpaid amount has occurred due to an incorrect amount of relevant income or wrong employee details being reported to us, please mark the correct information on the report so we can update our records.

Issuing pay records to employees

After making timely contributions with remittance statements, employers have to provide each employee with a pay record within 7 working days after the payment. The pay record should show the employee's relevant income, date of contribution paid to the trustee and the contribution amount for both mandatory and voluntary (if any) made by both employer and employee. If an employer fails to do so, a penalty may be imposed by MPFA. Refer to the MPFA website at www.mpfa.org.hk for details.

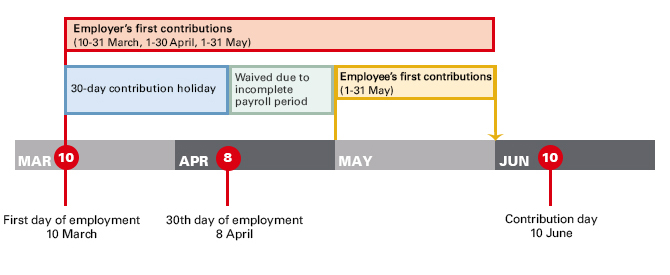

First contributions

As an employer, you have to make contributions for your employees from the first day of their employment. Your new employees, however, enjoy a '30-day contribution holiday'. That means, every new employee is not required to make contributions for the first 30 days of employment. Employees are also not required to make contributions for (i) any incomplete payroll period that immediately follows the 30-day period (if the employee's wage period is monthly or shorter than monthly); or (ii) the calendar month in which the 30th day of employment falls (if the employee's wage period is longer than monthly).

Below is a simple illustration for a monthly payroll cycle from the first day to the last day of the month.

Assumptions:

- Payroll cycle is on monthly basis, starting from the first day to the last day of the month

- A new employee joins on 10 March

The first contributions for new employees, including both employer's and employee's portions, have to be made on or before the 10th day of the calendar month after the last day of the calendar month on which the 60th day of employment falls. If the contribution day falls on a Saturday, public holiday, or gale or black rainstorm signal day, the contribution day will be postponed to the following business day that is not a Saturday, public holiday, or gale or black rainstorm signal day. However, it is not necessary to arrange MPF for employees who are employed for less than 60 days.

See below for the special dates for making first-time contributions for newly employed non-casual employees.

Pay attention to the special dates each year when enrolling and making first-time contributions for newly employed non-casual employees

Employers are obligated to enrol new employees into MPF schemes and make mandatory contributions in full on time. Otherwise, a financial penalty and/or surcharge may be imposed by the MPFA for late enrolment and/or late payment of contributions. It is essential to understand the MPF enrolment deadline into an MPF scheme and the correct day to make the first-time contributions for your newly employed non-casual employees.

First-time contributions:

The first-time contributions should be paid to your trustee on or before the 10th day after the last day of the calendar month on which the 60th day of employment falls.

However, there are some special days each year that employers should pay attention to. That is, when the MPF enrolment deadline falls on the last calendar day of a month which is a Saturday, a public holiday, a gale warning day or a black rainstorm warning day, making it necessary to extend the MPF enrolment deadline for the new employees to the first business day of next month. However, the 'first-time contribution day' for the first contributions of employee remains unchanged.

For instance, if the new employee's 60th day of employment is Saturday 29 April 2023, the enrolment deadline for this employee will be extended to next business day -- 2 May 2023 -- which is not a Saturday, a public holiday, a gale warning day or a black rainstorm warning day. However, there is no change to the end date of the permitted period (for the purpose of calculating the contribution day) and no postponement of the 'first-time contribution day', herein, the deadline for employer to pay the first-time contributions in full for this new employee remains unchanged on 9 May 2023.

Below shows the special dates in 2023, which share similar situation with the above example and employers should pay close attention to:

| Employment date |

The 60th day of employment |

Deadline for enrolment |

Correct first-time contribution day |

|---|---|---|---|

1 March 2023 |

29 April 2023 (Saturday) |

2 May 2023 (Tuesday) |

9 May 2023 (Tuesday) |

2 March 2023 |

30 April 2023 (Sunday) |

2 May 2023 (Tuesday) |

9 May 2023 (Tuesday) |

1 June 2023 |

30 July 2023 (Sunday) |

31 Jul 2023 (Monday) |

7 August 2023 (Monday) |

2 August 2023 |

30 September 2023 (Saturday) |

3 October 2023 (Tuesday) |

10 October 2023 (Tuesday) |

3 August 2023 |

1 October 2023 (Sunday) |

3 October 2023 (Tuesday) |

10 October 2023 (Tuesday) |

1 November 2023 |

30 December 2023 (Saturday) |

2 January 2024 (Tuesday) |

9 January 2024 (Tuesday) |

| Employment date |

1 March 2023 |

|---|---|

| The 60th day of employment |

29 April 2023 (Saturday) |

| Deadline for enrolment |

2 May 2023 (Tuesday) |

| Correct first-time contribution day |

9 May 2023 (Tuesday) |

| Employment date |

2 March 2023 |

| The 60th day of employment |

30 April 2023 (Sunday) |

| Deadline for enrolment |

2 May 2023 (Tuesday) |

| Correct first-time contribution day |

9 May 2023 (Tuesday) |

| Employment date |

1 June 2023 |

| The 60th day of employment |

30 July 2023 (Sunday) |

| Deadline for enrolment |

31 Jul 2023 (Monday) |

| Correct first-time contribution day |

7 August 2023 (Monday) |

| Employment date |

2 August 2023 |

| The 60th day of employment |

30 September 2023 (Saturday) |

| Deadline for enrolment |

3 October 2023 (Tuesday) |

| Correct first-time contribution day |

10 October 2023 (Tuesday) |

| Employment date |

3 August 2023 |

| The 60th day of employment |

1 October 2023 (Sunday) |

| Deadline for enrolment |

3 October 2023 (Tuesday) |

| Correct first-time contribution day |

10 October 2023 (Tuesday) |

| Employment date |

1 November 2023 |

| The 60th day of employment |

30 December 2023 (Saturday) |

| Deadline for enrolment |

2 January 2024 (Tuesday) |

| Correct first-time contribution day |

9 January 2024 (Tuesday) |

A First Contribution Calculator can help employers calculate the first-time contribution for their new employees.

Contributions for employees in other employment scenarios

Employees who reach the age of 18 or 65, or expatriates working in Hong Kong with an employment visa and the 13-month exemption period has ended

Employees who are below 18 years old or expatriates who enter Hong Kong for employment for less than 13 months are exempted1 from joining an MPF scheme. When these employees reached 18 or the 13-month exemption period ends1, the employer has to enrol them in an MPF scheme and make relevant mandatory contributions. The permitted period and '30-day contribution holiday' apply to employees in this situation.

Employees who reach 65 years of age and continue to be employed are not required to make mandatory contributions from the day they turn 65. Mandatory contributions for the concerned contribution period should be calculated up to the date before the employees reach the age of 65.

To report the contribution details for these employees by paper-based remittance statements, fill in the 'relevant income' and 'mandatory contributions' as follows:

- In the 'Relevant income' column

Provide the full relevant income (that is not the prorated relevant income) of the employee for the concerned reporting payroll periods.

- In the 'Mandatory contributions' column

Provide the actual mandatory contribution amount that should be paid by employer and employee respectively for the concerned reporting contribution periods.

Refer to the table below for examples in reporting the relevant income and mandatory contributions for the employees under the above 3 scenarios:

| Dates (YYYY-MM-DD) |

Payroll period (YYYY-MM-DD) |

Contribution period (YYYY-MM-DD) |

Relevant income | Employer's mandatory contributions | Employee's mandatory contributions |

|---|---|---|---|---|---|

| 2023-05-11 |

2023-05-01 - 2023-05-31 |

2023-05-11 - 2023-05-31 |

HKD23,0002 |

HKD23,000 x 21/31 x 5% = HKD779.033 |

Not applicable4 |

| 2023-05-11 |

2023-06-01 - 2023-06-30 |

2023-06-01 - 2023-06-30 |

HKD23,000 |

HKD23,000 x 5% = HKD1,150 |

Not applicable4 |

| 2023-05-11 |

2023-07-01 - 2023-07-31 |

2023-07-01 - 2023-07-31 |

HKD23,000 |

HKD23,000 x 5% = HKD1,150 |

HKD23,000 x 5% = HKD1,150 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

|---|---|

| Payroll period (YYYY-MM-DD) |

2023-05-01 - 2023-05-31 |

| Contribution period (YYYY-MM-DD) |

2023-05-11 - 2023-05-31 |

| Relevant income |

HKD23,0002 |

| Employer's mandatory contributions |

HKD23,000 x 21/31 x 5% = HKD779.033 |

| Employee's mandatory contributions |

Not applicable4 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

| Payroll period (YYYY-MM-DD) |

2023-06-01 - 2023-06-30 |

| Contribution period (YYYY-MM-DD) |

2023-06-01 - 2023-06-30 |

| Relevant income |

HKD23,000 |

| Employer's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Employee's mandatory contributions |

Not applicable4 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

| Payroll period (YYYY-MM-DD) |

2023-07-01 - 2023-07-31 |

| Contribution period (YYYY-MM-DD) |

2023-07-01 - 2023-07-31 |

| Relevant income |

HKD23,000 |

| Employer's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Employee's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Dates (YYYY-MM-DD) |

Payroll period (YYYY-MM-DD) |

Contribution period (YYYY-MM-DD) |

Relevant income | Employer's mandatory contributions | Employee's mandatory contributions |

|---|---|---|---|---|---|

| 2023-05-11 |

2023-05-01 - 2023-05-31 |

2023-05-11 - 2023-05-31 |

HKD23,0002 |

HKD23,000 x 21/31 x 5% = HKD779.033 |

Not applicable4 |

| 2023-05-11 |

2023-06-01 - 2023-06-30 |

2023-06-01 - 2023-06-30 |

HKD23,000 |

HKD23,000 x 5% = HKD1,150 |

Not applicable4 |

| 2023-05-11 |

2023-07-01 - 2023-07-31 |

2023-07-01 - 2023-07-31 |

HKD23,000 |

HKD23,000 x 5% = HKD1,150 |

HKD23,000 x 5% = HKD1,150 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

|---|---|

| Payroll period (YYYY-MM-DD) |

2023-05-01 - 2023-05-31 |

| Contribution period (YYYY-MM-DD) |

2023-05-11 - 2023-05-31 |

| Relevant income |

HKD23,0002 |

| Employer's mandatory contributions |

HKD23,000 x 21/31 x 5% = HKD779.033 |

| Employee's mandatory contributions |

Not applicable4 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

| Payroll period (YYYY-MM-DD) |

2023-06-01 - 2023-06-30 |

| Contribution period (YYYY-MM-DD) |

2023-06-01 - 2023-06-30 |

| Relevant income |

HKD23,000 |

| Employer's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Employee's mandatory contributions |

Not applicable4 |

| Dates (YYYY-MM-DD) |

2023-05-11 |

| Payroll period (YYYY-MM-DD) |

2023-07-01 - 2023-07-31 |

| Contribution period (YYYY-MM-DD) |

2023-07-01 - 2023-07-31 |

| Relevant income |

HKD23,000 |

| Employer's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Employee's mandatory contributions |

HKD23,000 x 5% = HKD1,150 |

| Dates (YYYY-MM-DD) |

Payroll period (YYYY-MM-DD) |

Contribution period (YYYY-MM-DD) |

Relevant income | Employer's mandatory contributions | Employee's mandatory contributions |

|---|---|---|---|---|---|

| 2023-05-21 |

2023-05-01 - 2023-05-31 |

2023-05-01 - 2023-05-20 |

HKD23,0002 |

HKD23,000 x 20/31 x 5% = HKD741.943 |

HKD23,000 x 20/31 x 5% = HKD741.943 |

| Dates (YYYY-MM-DD) |

2023-05-21 |

|---|---|

| Payroll period (YYYY-MM-DD) |

2023-05-01 - 2023-05-31 |

| Contribution period (YYYY-MM-DD) |

2023-05-01 - 2023-05-20 |

| Relevant income |

HKD23,0002 |

| Employer's mandatory contributions |

HKD23,000 x 20/31 x 5% = HKD741.943 |

| Employee's mandatory contributions |

HKD23,000 x 20/31 x 5% = HKD741.943 |

1 If the original period of an employee's employment visa for permission to work in Hong Kong is not more than 13 months, but the visa is renewed and brings the employee's total continuous period of permission for employment in Hong Kong to over 13 months, that employee would cease to be exempt from the first day after the 13-month period. No exemption will be given to an employee who has been granted an employment visa for permission to work in Hong Kong for a period of more than 13 months.

2 The relevant income reported on the remittance statement should be the full relevant income for the payroll period from 1 May 2023 to 31 May 2023 but not the prorated relevant income for mandatory contribution purposes for the contribution period.

3 The mandatory contributions reported on the remittance statement should be the actual mandatory contribution amount paid by the employer and/or employees for the contribution period. It's calculated using the prorated relevant income for the contribution period.

4 The first 30 days of employment and any incomplete contribution period or calendar month (depending on the remuneration cycle, eg weekly, monthly, quarterly) of the non-casual employee concerned) that immediately follows the 30-day period, during which the non-casual employees are not required to make mandatory contributions.

Contributions for retroactive salary adjustment

If the mandatory contributions of a previous contribution period of your employees having been fully settled on or before the relevant contribution day according to the relevant income stated in the remittance statement at that time, but if there is a subsequent change of the employee's relevant income resulting in an increase of the mandatory contributions for such contribution period, as the increased part of mandatory contributions cannot be settled on or before the relevant contribution day of the previous contribution period, it will be considered as a default contributions. Trustees will have to report the default contributions to the MPFA.

Retroactive salary adjustment is a common practice in many industries. To avoid default contributions due to improper reporting of salary adjustment, you should report relevant income and make mandatory contributions properly when making a back payment of salary to your employee.

Proper reporting of the relevant income and contributions

Back payments (eg payments relating to an earlier period perhaps arising from a salary adjustment or a time lag between the ascertainment and payment of commissions, tips or bonuses) to a relevant employee are not relevant income, in general, until the contribution period in which the back payment is ascertained and paid.

For example, an employer decides to increase the salary of an employee in September in a particular year, the relevant salary adjustments can be traced back to 1 April of the year, the amount of the increased salary of April, May, June, July and August of that year should be included in the relevant income of September as and when the back payment are ascertained and paid.

If the employer adjusted the relevant income and mandatory contributions of each contribution period from April to August, despite the increased part of mandatory contributions were immediately paid, the increased part of contributions will still be regarded as not been paid on or before the contribution day of the relevant contribution period. As employers are required to settle the mandatory contributions in full on or before the contribution day of the relevant contribution period, MPFA may impose a surcharge and/or financial penalty of these late contributions on the relevant employers.

| Contribution periods |

Contribution periods |

|

|---|---|---|

| April/May/June/August |

September |

|

| Proper reporting of relevant income and contributions |

No adjustment of the relevant income and employer's and employee's mandatory contributions for each contribution period |

Report and settle the following mandatory contributions:

Relevant income: HKD22,000 (include the salary of HKD12,000 for September 2023 and increased part of salary HKD2,000 each month, totalling HKD10,000 from April to August)

Employer's mandatory contributions: HKD1,100

Employee's mandatory contributions: HKD1,100 |

| Improper reporting of relevant income and contributions (Additional mandatory contributions may subject to surcharge and/or financial penalty imposed by MPFA) |

Adjust the relevant income for each contribution period: HKD10,000 to HKD12,000

Adjust both employer's and employee's mandatory contributions for each contribution period: HKD500 to HKD600

Pay the total additional employer's and employee's mandatory contributions amount: HKD1,000 |

Report and settle the following mandatory contributions:

Relevant income: HKD12,000

Employer's mandatory contributions: HKD600

Employee's mandatory contributions: HKD600 |

| Contribution periods |

September |

|---|---|

|

Proper reporting of relevant income and contributions |

|

| Contribution periods |

Report and settle the following mandatory contributions:

Relevant income: HKD22,000 (include the salary of HKD12,000 for September 2023 and increased part of salary HKD2,000 each month, totalling HKD10,000 from April to August)

Employer's mandatory contributions: HKD1,100

Employee's mandatory contributions: HKD1,100 |

|

Improper reporting of relevant income and contributions (Additional mandatory contributions may subject to surcharge and/or financial penalty imposed by MPFA) |

|

| Contribution periods |

Report and settle the following mandatory contributions:

Relevant income: HKD12,000

Employer's mandatory contributions: HKD600

Employee's mandatory contributions: HKD600 |

| Contribution periods |

Contribution periods |

|

|---|---|---|

| April/May/June/August |

September |

|

| Proper reporting of relevant income and contributions |

No adjustment of the relevant income and employer's and employee's mandatory contributions for each contribution period |

Report and settle the following mandatory contributions:

Relevant income: HKD32,000 (include the salary of HKD22,000 for September 2023 and increased part of salary HKD2,000 each month, totalling HKD10,000 from April to August)

Employer's mandatory contributions: HKD1,5001

Employee's mandatory contributions: HKD1,5001 |

| Improper reporting of relevant income and contributions (Additional mandatory contributions may subject to surcharge and/or financial penalty imposed by MPFA) |

Adjust the relevant income for each contribution period: HKD20,000 to HKD22,000

Adjust both employer's and employee's mandatory contributions for each contribution period: HKD1,000 to HKD1,100

Pay the total additional employer's and employee's mandatory contributions amount: HKD1,000 |

Report and settle the following mandatory contributions:

Relevant income: HKD22,000

Employer's mandatory contributions: HKD1,100

Employee's mandatory contributions: HKD1,100 |

| Contribution periods |

September |

|---|---|

|

Proper reporting of relevant income and contributions |

|

| Contribution periods |

Report and settle the following mandatory contributions:

Relevant income: HKD32,000 (include the salary of HKD22,000 for September 2023 and increased part of salary HKD2,000 each month, totalling HKD10,000 from April to August)

Employer's mandatory contributions: HKD1,5001

Employee's mandatory contributions: HKD1,5001 |

|

Improper reporting of relevant income and contributions (Additional mandatory contributions may subject to surcharge and/or financial penalty imposed by MPFA) |

|

| Contribution periods |

Report and settle the following mandatory contributions:

Relevant income: HKD22,000

Employer's mandatory contributions: HKD1,100

Employee's mandatory contributions: HKD1,100 |

1 Subject to the maximum level of relevant income for MPF contributions. Example 2 is illustrated using the maximum mandatory contributions amount of HKD1,500 per month.

Smart Tips

Failure to report contribution details and make MPF payments in full on or before the relevant contribution day may result in defaulting on MPF contributions or surcharges, which is a criminal offence. Visit the MPFA website at www.mpfa.org.hk for details and impact of non-compliance with MPF legislative requirements.